Excavators And Loaders: Small Machines Are Digging The Market Out Of The COVID Hole

May 31, 2021 - 5 years ago

As part of the latest off-highway vehicle market report, the researchers at Interact Analysis have presented an insight into likely market performance in the earthmoving equipment sector. As with the rest of the off-highway vehicle sector, the COVID-19 pandemic caused severe market contractions in 2020 for the earthmoving sector.

Excavators and wheel loaders, the specific focus of this insight, for example, saw negative growth in Europe of -22% and -16% respectively. But looking to the future, the outlook looks positive for the mini- and medium excavator markets, and the market for compact wheeled loader machinery also looks healthy. Larger machinery will see a more sluggish recovery and market growth.

Small Excavator Growth To 2029

Excavators have a higher predicted growth rate than loaders. Hydraulic excavators have become particularly popular in a range of settings, and they are replacing wheeled loaders in coal mines. Meanwhile, mini-excavators are gradually replacing backhoe loaders, an earthmoving concept which has been around since the 1950s. The mini-excavator market was the first earthmoving sector to see a post-COVID-19 recovery, which was detected in 4Q 2020. There is strong demand for these machines in North America and China and their share of the global excavator market is predicted to rise from 44.8% in 2019 to 49.3% in 2029. Medium excavators are also expected to see sustained growth, but their initial recovery will be slower and, while the mineral extraction sector continues to be badly affected by COVID-19, the large excavator market will lag behind.

China’s race to modernize and extend its infrastructure to support its burgeoning economy has made it the biggest regional market for excavators. In 2019, 35% of global excavator sales went to China, with Europe in second place on 21%. As an interesting comparator to this, during 2020 China’s market share rose to 47.6%, as China bucked the trend, being the only region where the excavator market saw year-on-year growth (37%). We expect China’s demand for excavators to remain strong going into 2021, though the growth rate is likely to flatten a little.

Predictably, demand for larger excavators is greater from emerging economies where there are more major infrastructure projects. Conversely, developed countries such as the US, Japan, Germany, and France currently account for 60% of the mini excavator market, where these machines are usually purchased by rental companies and are rented out for use in urban settings where modernization projects are often executed in enclosed environments.

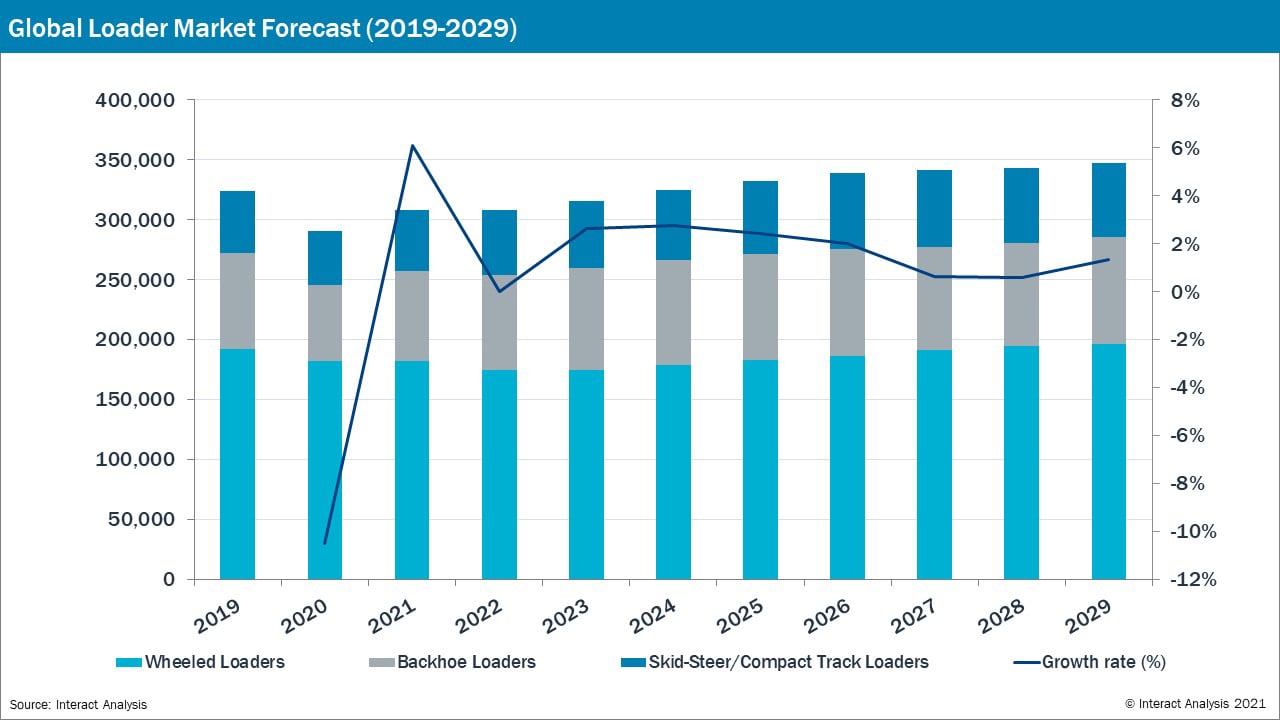

Investment In Loaders: Post-Covid Surge, Then Stability

As construction activity picks up across the globe, demand for compact machinery such as skid steer loaders and compact wheeled loaders is increasing. A surge of investment in anticipated in loader equipment over the course of 2021, with a consequent dip in 2022, followed by a slight rise and overall levelling off as the market stabilizes.

As illustrated in the above chart, wheeled loaders – which are used widely across all regions, but with China accounting for over 50% of the market – are predicted to consistently occupy the largest market share. And, as with excavators, it is compact machinery that will see the greatest demand, particularly in developed countries (Germany, France and Japan accounted for 75% of compact wheeled loader shipments in 2019). However, there isn’t as much demand for compact machinery in developing markets such as South America and South Asia, as infrastructure projects grow. Skid steer loaders are forecast to see gradual growth up to 2029, their principal market being North America, which has accounted for 80% of sales of these machines. The Backhoe loader market, where India has accounted for almost a 50% share, remains consistent and significant throughout the forecast period. Low interest rates in Europe and tax subsidies encouraging the replacement of old machinery with new energy vehicles have given contractors the confidence to invest in new loader equipment in Europe. Additionally, stringent emissions standards are driving the market for electrified compact wheeled loaders.

Full Electric And Hybrid Making Inroads, But It’s A Slow Process

As with most vehicles, so it is with earthmoving machines: the larger they are, the more difficult it is to insert a practicable alternative energy solution owing to issues around battery capacity, range, charging infrastructure, and down-time for charging. That said, as most large machinery is used in environments where emissions controls are less strict, i.e. in out-of-town settings, the impetus to electrify is much weaker. It is forecasted that around only 6.2% of all large excavators (30+ tons) sold globally in 2029 will be electrified. New energy solutions for medium sized excavators (20+ tons), having centered so far around the concept of the hydraulic hybrid swing, are showing signs of extending into full electric options, with companies such as Volvo and Komatsu researching the technology. But, for excavators, the category most likely to see a real push for electrification is the mini excavator, the machine often being used in environments where noise and pollution controls are stringent. There are already thousands of these battery-electric machines in commission currently, such as the Volvo ECR25 Electric, and it is forecasted that the penetration rate for electrified powertrains for these smaller machines will stand at a significant 18.6% by 2029. Overall, it is forecasted that by 2029, 13% of global excavator sales will be of full electric machines.

Predictably, the outlook is similar for compact wheeled loaders, where there will be higher rates of electrification as compared to large machines. The Kramer 5055e, currently available in the EU, is an example. The push to improve efficiency and reduce costs in larger wheeled loaders may in fact lead to a general scaling down in the average size of these machines, enabling electrification, which will in turn reduce the number of components in the machines, resulting in less wear and tear and maintenance work, which all incurs a price.

Share this article!

News Archive

-

2026

-

July

- Wirtgen Now Offers Vario Impact Sizer

- Hultdins Phases Out Select SuperGrip II Grapples

- Dynaset Celebrates 40 Years Of Innovation

- Metso Launches New Primary Crushers

- LGP vs Standard Track Dozers: Which Undercarriage Fits Canadian Ground Conditions?

- Caterpillar Launches Three New Compact Machines

- LGMG Introduces New High-Performance Telehandler

- Skyjack Launches New Slab Booms

- 5 Ways To Enhance Railway Vacuuming

- Finlay Launches I‑130 and I‑130RS Impact Crushers

- New Cat 308 CR Fixed Boom Mini Excavator

- Terex Washing Systems Introduces New AggreScrub P80

- JLG Previews New 600AJ+ Boom Lift

- Sennebogen Introduces New Steering Tech For Telehandlers

- Vermeer Details VX75 Vacuum Excavator Configuration Options For Utility Contractors

- AWD vs Tandem Drive Motor Graders: Which Setup Fits Snow, Gravel Roads, and Rural Maintenance?

- Trucks For Change Network Packs Snacks for Kids Across Canada

- VMAC Recognized as One of Canada’s Best Managed Companies for 2026

-

June

- Vallée Introduces Its New 4DA5E Articulated Rough-Terrain Forklift

- New TS160-4 Pneumatic Tire Roller From Sakai

- Supply Post July 2026 Issue – Read it now!

- Volvo CE Adds Short-Swing ECR255 Excavator

- Stellar Introduces Redesigned Large OTR Tire Truck

- 20-Tonne vs 30-Tonne Excavators: Which Size Makes Sense for Canadian Contractors?

- Daimler Brought Latest Innovations To Truck World 2026

- Link-Belt Excavators Presents $232,000 to Breast Cancer Organizations

- 7 Ways To Simplify Sewer Cleaning

- Tigercat Introduces New 820 Series

- KOBELCO Introduces The SK1300DLC-11

- Dynapac Bids Farewell To Last SD2500CS Large Paver

- DEVELON Introduces -9 Series Crawler Excavators

- BC Supports Wood-Waste Innovation In The Kootenays

- John Deere Adds New X-Tier Wheel Loaders

- Magnum Trailer Joins Merritt Family

- WorkSafeBC Reminds Employers To Prepare For Summer Weather Hazards

- 4x4 and Extendahoe Backhoes: Which Options Are Worth Paying For in Canada?

- Kryton Brings Its Innovative Construction Technologies to the Mining Industry

- Queclink Launches High-Spec Trailer Tracking Solution

- Celebrating 10 Years Of The Liebherr R 9200 Excavator

- A Trucker's Tale – Misadventures In Hauling: Coiled Wire Rod Edition

- Kobelco Introduces Next Generation SK850LC-11 Excavator

- FLO Components Ltd. Announces Winner in NHES Lincoln 1888 PowerLuber Grease Gun Contest

- Volvo Launches New SD70 Soil Compactor

- Hangcha Forklift Canada Strengthens Quebec Presence

- Case IH Launches Nutri-Tiller 1000 Series

- Gray Tools Supports Skilled Trades Education

- Peterbilt Reinforces Commitment to Canadian Market

- Fuel Transport Named Coca-Cola’s Canadian Carrier of the Year

- CASE CE Authorized Dealer Network Change In Ontario

- Volvo Launches New Electric Trucks

- Single Autonomous Class 8 Truck Trial Complete

- New Cat Orange Peel Grapple And Bucket Attachments

- Freightliner Adds Digital Dash To Cascadia

- Articulated vs Rigid Off-Highway Trucks: Choosing the Right Hauler for Canadian Job Sites

- Hydrogen-Fueled Trucks Are Here

- Wabash Unveils Next-Generation Cargo Assurance Solution

- Daimler Truck Celebrates 130 Years

- Caterpillar Updates AP Pavers

- Standard Flow vs High Flow Skid Steers: What Canadian Buyers Should Check Before Paying More

- New NPK Dealer In Ontario

- SAKAI Adds New Dealer In Canada

- Alberta Equipment Expo Returns In 2027 Bigger Than Ever

- MAJOR Showcases Innovative Screen Media Solutions

- EvoQuip Celebrates 10 Years

- Doppstadt Introduces New SWS 6 Spiral Shaft Separator

- Alliance Concrete Pumps Expands Aldergrove Facility

- Epiroc Extends Warranty For Selected Excavator Attachments

- Eagle Iron Works Launches Hawk Fines Recovery Plant

- Terex Launches TRAC Vibration Analysis System for Screening Equipment

- Unique ABG Screed Delivers High Performance

-

May

- Powerscreen Celebrates 60 Years of Mobile Screening At Hillhead 2026

- Craig Manufacturing Acquires Intellectual Property of 4-D Welding & Fabricating

- Supply Post June 2026 Issue – Read it now!

- Alberta Is Reducing Trucking Barriers

- Unlock More Tonnage from Your Primary Crusher with Heavy-Duty Jaw Profiles

- Trail King Introduces New Steering Trailers

- Mack Trucks Debuts New Windshield Technology

- Used Excavator Hours: When a High-Hour Machine Is Still Worth Buying

- McLanahan Launches New Products

- Epiroc Presents New EC 122 Hydraulic Breaker

- Finlay Introduces New Impactors

- Astec Launches The A50 Jaw Crusher

- Talking Tailgates

- Komatsu Becomes First OEM To Commission 1,000 Ultra-Class Autonomous Haul Trucks

- Wheel Loader Tires, Buckets, and Couplers: Small Details That Change the Real Cost of Ownership

- How Buckets Stop Hard Waste Rock Contamination

- Vermeer Launches New TR6500TX Tracked Trommel Screen

- Now Accepting Applications: BCTA Scholarships for 2026

- A Trucker's Tale – Management Woes

- New Tracked Carriers From FAE

- SANY Excavators Built For Tough Jobsites

- New Holland Introduces All-New T7 XD Tractor

- Bobcat Introduces New Batteries For Electric Sit-Down Forklifts

- New 6040 Mining Shovel From Caterpillar

- Truck-Lite Previews New Trailer Back Up Safety System

- Used Dozers with Grade Control: Benefits, Risks, and Buying Checks

- Epiroc Launches Three All-New Electric Pit Viper Drills

- Generac Introduces New Diesel Generators

- GLS Canada Chooses Orange EV HUSK-e Trucks

- TrafFix Devices Introduces Water Cable Barrier

- Roadbuilding Success Using Crusher Buckets

- Harbour Air Takes Off with Major Network Expansion

- Compact vs. Mid-Size Wheel Loaders: Choosing the Right Size for Canadian Contractors

- Hyster Launches Revolutionary New Lift Truck Automation Solution

- New HRVB-HD Hydraulic Recycling Vacuum Bucket From Dynaset

- Techniques For Cleaning Around Obstacles With Street Sweepers

- SANY Builds Landscaping Machines For Fast, Finish-Critical Work

- New Cat 6015 Mining Shovel

- International Launches Level 4 Autonomous Fleet Trial

- 2-Speed Travel, Ride Control, and Air Ride Seat: Which Skid Steer Features Are Worth Paying For?

- Volvo CE Updates Next-Gen A60 Articulated Hauler

- Detroit introduces 2027 Heavy-Duty Gen 6 Engines

- New Cab For Vermeer D24 Horizontal Directional Drill

- Merlo Introduces New ROTO Plug-In Telehandlers

- BCCSA Opens Applications for Second Year of Bursary Program to Support Careers in Construction Safety

- Short Tail Swing vs Conventional Excavators for Urban Utility Work in Canada

- Tigercat Updates 6040 Carbonizer Permitting Progress

- Supply Post May 2026 Issue – Read it now!

-

April

- DEVELON Introduces New DX340LL-7 Log Loader

- Ecotec Introduces The New TSS 390 Plus Shredder

- New Products From SDLG

- New TI5064 Impact Crusher From Cedarapids

- Box Heat, Tailgate, Auto Grease, and Backup Camera: Which Off-Highway Truck Options Matter in Canada?

- The National Heavy Equipment Show Wraps Up Momentous 30th Anniversary Edition

- Caterpillar launches New 319 Compact Radius Excavator

- New HM460-6 Articulated Truck From Komatsu

- Bron Expands Ontario Facility

- CASE Announces New Graders

- Hydraulic Thumb, Quick Coupler, and Auxiliary Hydraulics: Which Excavator Setup Actually Saves You Money?

- Maximizing Industrial Cleanup Productivity

- Waratah Introduces New FL90 Directional Felling Head

- ProStack 150 ft Telescopic Conveyor Takes Terex To New Heights

- Komatsu Introduces New Excavators

- Kleemann Launches New MOBISCREEN MSS 1102 PRO Mobile Scalper

- Skyjack Launches New SJ5545 E Slab Scissor

- JLG Adds AUSA Equipment to Growing North American Product Portfolio

- Velocity Trailer Centers Expands Vanguard Trailer Availability

- Introducing The New Cat D8 XE Dozer

- Astec Launches New Peterson 3710E Horizontal Grinder

- New Holland Introduces New Electric Compact Machines

- Link-Belt Debuts 245 X4S Excavator

- Mid-Size Used Dozers in Canada: When to Buy a D4/D5 Class Machine vs Moving Up to a D6 or D8

- Peterbilt Reinforces Commitment to Canadian Market at Truck World 2026

- Frontline Machinery Launches Frontline Washing Systems

- Volvo CE To Close Rokbak Business

- Tigercat Revamps 568 Harvesting Head

- Connecting Canada Coast To Coast

- A Trucker's Tale – Characters I Have Known

- Supply Post Joins ICBA

- Cat Introduces New Motor Graders

- Cedarapids Launches CRH5064 Portable HSI Impactor Plant

- Mack Keystone Makes World Debut

- Tigercat Debuts New 6440 Chipper

- Metso And Nors Expand West

- Motor Grader Size Classes Explained: Matching Horsepower and Blade Width to Your Application

- Fuel Transport Adds Dedicated Fleet Footprint Option For GTA

- How To Keep Hydro Excavation Trucks Running Their Best

- Detroit Launches New DT12-VL

- JLG Introduces New 860SJ+ Boom Lift

- Volvo CE Brings Next-Gen Wheeled Excavators To North America

- Mack Trucks Introduces All-New Granite

- Kenworth Introduces The C580

- Stoughton Adds TyCorra Fleet Solutions As Dealer In Eastern Canada

- Vermeer Introduces New Vacuum Trucks

- Rototilt Celebrates 40 Years

- Two New Skid Steer Attachments From Loftness

- Queclink Develops Satellite-Enabled Vehicle Tracking

- Canadian Concrete Expo 2026 Sets New Records

- Euro Auctions Group Delivers Strong March Performance

- Why Your Dozer Always Breaks Down on the Last Day of the Job

- BOMAG Launches New BT 30 Tamper

- Tesab Introduces New 623TR Impact Crusher

- Supply Post April 2026 Issue – Read it now!

-

March

- Three Weeks Remain Until the Return of the National Heavy Equipment Show

- Heil Trailer Marks 125 Years

- Manitoulin Transport Opens New Moncton Terminal

- Atlantic Heavy Equipment Show Wraps Momentous Edition

- Volvo Unveils The New EC950 High Reach Demolition Excavator

- Anaconda Equipment Launches The I14R Impact Crusher

- Rebar Recovery Using Crusher Buckets

- Kenworth Introduces New Medium Duty Battery-Electric Trucks

- Ammann Unveils New Colors for North American Machines

- Mack Trucks Launches New Vocational Models

- What Happens In Vegas, Stays In Vegas…Or Does It?

- Atlantic Canada’s Largest Heavy Equipment Show Opens 40th Anniversary Edition Today

- Radial Lift vs. Vertical Lift Skid Steers. How the Boom Design Changes What You Can Do

- Bobcat Unveils New Compact Loaders

- Gradall Introduces New XE 4100 Excavator

- New Holland Adds New D-Series Mini Excavators

- GOMACO Introduces Revolutionary Polymer Paver

- First Look At Two Next-Generation Dozers From Komatsu

- Rokbak Trucks Cement Trust In Canada

- Brigade Demonstrates Latest Vehicle Safety Solutions

- DEVELON Debuts Next-Generation Excavators

- FLO Components Ltd. Showcases RecondOil Technology

- Weaver Auctions Joins Euro Auctions Canadian Network

- Dozer Blade Types Explained: S-Blade, SU-Blade, U-Blade, and PAT - Which One Do You Actually Need?

- A Trucker's Tale – Bored In Baltimore

- 2026 Atlantic Heavy Equipment Show Guide is here!

- John Deere Enters New Era Of Excavators

- Terex Washing Systems Launches New FM 300 Compact

- Volvo CE Launches Three New-Gen Compact Excavators

- JLG Introduces ES2632M Micro-Sized Scissor Lift

- Case IH Launches New Farmall Compact Tractors

- BC’s Wildfire Future Needs Forest Professionals

- Excavator Configurations for Demolition Work: What to Look For Beyond Weight Class

- Ammann Launches New Forward-Moving Vibratory Plates

- Forests Canada Passes 7 Million Tree Milestone In Ontario Greenbelt

- Zero-Emission Trucking Testbed Report Released

- Forestry Is a Solution: Voice Your Support

- Peterbilt Introduces Electronic Parking Brake For Class 8 & Medium Duty Vehicles

- 2025 A Banner Year For Wildfire Salvage

- New Grapple Designs From Hultdins

- FPAC and Canada Wood Welcome Renewed Canada–China Cooperation

- Sandvik Invests In New Manufacturing Facility In Greater Sudbury

- Canadian Wood Council Advances Wood Innovation and Education

- February 2026 Canadian Equipment Market Insights

- The Silviculture Innovation Program and the Forest Enhancement Society of BC Launch New Extension Specialist Role

- A New Digital Service From Ponsse Monitors Logging Emissions

- Super-Heavy Loads Affect Travel In Edmonton Region

- Wabash Launches Trailers As A Service

- MAXAM Tire Introduces New MSV01 PRO

- Doppstadt Brings Redback Horizontal Grinders To North America

- Tigercat Releases Convertible Mulcher Carrier

- Significant Upgrades For Liebherr Gen 8 Crawler Excavators

- Tigercat Begins Production Of H-Series Feller Bunchers

-

February

- Supply Post March 2026 Issue – Read it now!

- Meet The Tree Nursery Growing Future PEI Forests

- Alamo Group Acquires Petersen Industries

- Production Begins Of All-New Mack Anthem

- Yukon Announces New Forest Sector Fund

- Safety Advice For Mulching Attachments

- Lode King Introduces Distinction RG Series For 2026

- Complete Excavator Price Guide for Canada (2026 Updated)

- Foreman Equipment Strengthens Customer Support with Terex Gold Level Train-the-Trainer Certification

- CTNA Sounds Alarm Over Critical Tree Seedling Shortage

- Trade Show Season Is Back And Better Than Ever!

- CBI Promotes CBI 5900T Horizontal Grinder At Conexpo

- The Hidden Cost of Hauling: How On-Site Air Curtain Burners Reduce Transport Emissions

- Quadco Introduces New M42 Mulcher

- Task Force Begins Work To Transform Canadian Forestry

- John Deere Introduces New L-III Wheeled Feller Bunchers

- Komatsu Introduces XF895-3 Forwarder

- A Trucker's Tale – Slick Nick

- Report Calls For Fundamental Shift In BC Forest Management

- Rigid Reveals New Phoenix Series Lights

- Komatsu Integrates engcon Tiltrotators

- TrafFix Devices Highlights Urbanite Pedestrian Wall

- A New Era For AUSA With JLG

- Metso Introduces A Groundbreaking Life Cycle Services Model For Minerals Processing

- Maximum Excavation Equals Maximum Production

- Hamm Launches New HC 130i C VA Compactor

- JCB Launches Two New Compact Units

- Ultimate Guide to Buying Construction Equipment in Canada

- Felling Directional Drill Trailers: Safety In The Field

- Celebrating 50 Years Of Nordberg C Series Jaw Crushers

- Sand, Gravel, And Woman Power For Kleeman Screening Plants

- No Futility For Utility Contractors

- January 2026 Equipment Market Insights

- Super-Heavy Load Affects Travel In Northeast Alberta

- Bobcat Introduces New Compact Excavators

- The Agri Pivot: A Versatile Telescopic Wheel Loader

- Perkins Launches 2806F-E18TAG2 ElectropaK Engine

- Winnipeg To Be Future Home of Gate

- Peterbilt Celebrates 100,000th Model 567

- FAE Launches New PT300 D:MINE Demining Vehicle

- JLG Marks Year Of Growth In North America

- Cedarapids Launches CRH5064 Portable HSI Impactor Plant

- Brokk Celebrates 50 Years As Pioneers In Demolition

-

January

- CCLS Opens New Logistics Facility In Mississauga

- Supply Post February 2026 Issue – Read it now!

- Street Sweeping In Various Climates: What To Know

- New VSE Tornado Screening Buckets From Simex

- Bobcat PG1140 Combines Power and Portability in One Rugged Trailer

- Merlo Introduces New Telehandler

- International Begins Autonomous Fleet Trials

- Sandvik Invests $51M CAD In New Saskatoon Facility

- Anaconda Equipment Expands Dealer Network With Skreenquip Partnership

- Fecon FTX150-2: A Powerful Firefighting Ally

- CTA Launches Stop Illegal Trucking Campaign To End Industry Lawlessness

- Registration Now Open For 2026 National Heavy Equipment Show

- Komatsu Introduces New PC365LC-11 Excavator

- BC Releases Independent Review Of CleanBC

- Kubota Canada Expands Construction Lineup

- From The Archives: The Flea Circus

- Supply Post's Toll-Free Phone Number Has Been Found!

- A Trucker's Tale – To Be Frank

- From the Archives: Tilt Deck Trailer Innovation On Vancouver Island

- Alberta Plans Reforms For Sand And Gravel

- Goodyear Launches Search For The Most Heroic Truck Drivers

- Peterbilt Delivers First Model 567 Built in Canada to Environmental 360 Solutions

- New Holland Introduces T7.270 Methane Power Tractor

- HD Hyundai Launches HT38 CTL Track Loader

- Vermeer Expands Microtrenching Solutions

- Guzzler Revolutionizes Offloading Solutions

- Bobcat Introduces EA Series Variable Speed Industrial Air Compressors

- Leasing vs. Buying Heavy Equipment: What’s Best for Your Business

- Setting Up Sewer Systems For Success In The New Year

- Tigercat Announces 5185B Enhancements

- More Options In Ontario For Stargate Trailers

- Brandt Showcases Expanded Lineup of Heavy Haul Trailers at NTDA Convention

- Canada's First Hydrogen-Powered Grocery Delivery Truck

- Caterpillar Updates Mini Excavators

- Large Loads Affect Travel In North Central Alberta

- MAGNA Strengthens North American Footprint with Molson US Powerscreen

- JLG Introduces New R13100 Telehandler

- New Guide Will Help Employers Build A Policy For Automated External Defibrillators

- December 2025 Canadian Equipment Market Insights

- Cat Introduces New Track Clamp Master Link

- Komatsu Unveils Historic P&H 2100BL Shovel Monument

- Nors Appoints New National Leadership For Canadian Market

- Towmaster Launches New T-30D Triple-Axle Drop-Deck Trailer

- Bandit Announces Centrifugal Clutch Option 12XC Woodchipper

- Registration Now Open for 2026 Atlantic Heavy Equipment Show

- Vactor Releases Dual Hose Reel For Ramjet Trailer

- Ammann America Expands Dealer Network in Ontario and Quebec

- Freightliner Cascadia Takes Spaceplane One Step Closer to Orbit

- Gomaco Introduces Revolutionary GP348 Paver

-

July

-

2025

-

December

- Kleemann Plant Train Delivers Two Material Specifications

- Supply Post January 2026 Issue – Read it now!

- John Deere Redesigns Two Compact Excavators

- Tigercat Rebrands Attachments Line To TCi

- Meet A Recycling Powerhouse: The Lippmann 3062 Jaw Crusher

- Komatsu Introduces XF895-3 Forwarder

- Supply Post Holiday Hours

- Canadian Combine Sales Soar In August

- Genie Expands Optional Accessories For Boom Lifts And Scissor Lifts

- AEM Unveils Comprehensive Study On Water Utilization

- Nors Now Distributes Manitowoc Mobile Cranes

- Announcing The 28th Annual Pacific Agriculture Show

- Peterbilt Introduces All-New Medium Duty EVs

- From the Archives: Harrison Makes A Comeback

- Tyalta Industries Announced as ProStack Distributor for Western Canada

- From the Archives: Butler Takes Volvo Line

- A Trucker's Tale – Trucking Stories

- 55 Years, Eh?

- Astec Introduces New EZR3 Screed

- Skyjack Scissor Lift Put To Work At University Of Guelph Alumni Stadium

- Indeco HP 7000 Successfully Tackles Tough Quarry Challenges

- Tigercat Introduces High Performance X877 Buncher

- ESCO Introduces New CycloBurst Barrel

- LiuGong Unveils Flagship Forklift

- Komplet Celebrates 25 Years of Innovation

- Manitoulin Acquires Martin Roy Transport

- November 2025 Canadian Equipment Market Insights

- Manitou Launches New Large-Frame Loaders

- Alberta Puts The Brakes On Predatory Towing

- Celebrating the 850,000th Western Star Built

- FAE Introduces New RCU45 Ultra-Compact Tracked Carrier

- Super-Heavy Load Affects Travel In Northeast Alberta Dec 9-10

- LBX Company Announces 145 X4S Excavator

- EvoQuip Expands Jaw Crusher Range With Bison 220 & 220R

- Cat Introduces Smarter Articulated Trucks

- Finlay Launches New 693 & 694 Inclined Screeners

- MDS Marks 30 Years In Business

- Brandt Opens New Grande Prairie Truck & Trailer Facility

- Samsara-Trucking HR Canada Top Fleet Employers scholarship applications now open

- Vermeer Launches New ML Series Mini Loaders

- Working From A Distance With Hydro Excavation

- Bobcat Unveils Its Most Powerful Small Articulated Loader

- Hyster Expands UT Line

- John Deere Introduces New L-III Skidders

- Hitachi Announces New Brand Name: Landcros

- Supply Post December 2025 Issue – Read it now!

-

November

- Large Loads Impact Travel In North Central Alberta

- Cat Introduces Next Gen Backhoe Loaders

- Komatsu Opens New Full-Service Parts Distribution Center In Edmonton

- Mack Debuts All-New Mack Anthem

- Calling All Future Pros: DEWALT Trades Scholarship Now Accepting Applications

- Telestack Launches TCL 2031 Track Mounted Conveyor

- Tigercat Upgrades 850 Series Processor

- Rokbak Haulers Worth Their Weight In Gravel For Alberta Crew

- Lippmann & Maverick Expand Partnership

- Kubota Canada Launches Grand L70 Series Compact Tractors

- A Quarry Story: Liebherr Crawler Excavator R 992

- LBX and Equipment Sales & Service Win First Place at the 2025 Global Skills Contest

- Nors Donates Volvo L25 Wheel Loader For Sustainable Housing

- IEOA Announces 26th Annual Truck Parade & Food Drive – December 6, 2025

- Western Star Hauls A Giant Of The Skies

- The 2025 Supply Post Christmas Shopping Guide

- A Trucker's Tale – Staying Awake

- Thermo King Expands TE Series For Electric Buses

- Maxam Tire Adds New 45/65R45 To The MS501 L5 Series

- Allison Transmission Monitoring Now Available Across All Mack Powertrains

- Bridgestone Launches V-Steel Highway Service 3 Crane Tire

- Bridgestone Launches New Firestone FS592 Trucking Tire

- Stoughton Trailers Unveils Next-Generation Intermodal Container

- A Perfect Pairing: Allison Transmission 4500 RDS Model + Cummins

- Bendix ADB22X Air Disc Brake Marks 20 Years

- Loftness Introduces Hydraulic Cooler For New Kubota Track Loader Model

- FAE MTL Multitask Head Now Available For Tractors Up To 300 Hp

- New Bendix Fusion Now Available On Kenworth T680s

- MAXAM Tire Expands AgriXtra Line

- The Critical Role Of Vacuum Trucks In Post-Disaster Cleanup

- Epiroc Introduces Automatic Bit Changer

- Sandvik Introduces Newtrax Control Room Editor

- Alamo Group Opens New Facility In Caledon

- Freightliner M2 Plus Models To Feature LED Headlights

- Engcon & Develon Join Forces To Launch Tiltrotator-Ready 9 Series Excavators

- New Cat C32B Engine Delivers High Power Density and Improved Durability

- Offset Helix Rotor Design Sets Industry Standard

- Canadian Concrete Expo Expands For 2026

- New Lifting Points From Pewag

-

October

- Super-Heavy Load Impacts Travel In Northeast Alberta

- Tele Radio Enhances Safety For VDL Container Systems

- Supply Post November 2025 Issue – Read it now!

- Liebherr Launches Unicontrol On G8 Crawler Dozers

- FAE App Can Reposition RCU Vehicles

- Software Updates For Cat 303.5 CR Mini Excavator

- New RH9 Rock Drill Head From Vermeer

- Indeco IMH Hydraulic Mulchers Ideal For Clearing

- A Bucket for All Jobs

- New Holland Launches myNewHollandConstruction Telematics

- Waratah Launches New H427 & H427X Harvester Heads

- A Heavy Equipment Spring Is Coming!

- Mulching Tips And Strategies For Post-Fire Cleanup

- CPKC 2025 Holiday Train Kicks Off Nov. 19

- A Trucker's Tale – Hit and Run!

- New G-Tier Rollers From Hamm Ideal For Rentals

- Kobelco And Trimble Announce Expanded Collaboration

- Fecon Introduces New Stone Crusher Series

- Case IH Unveils Steiger 785 Quadtrac

- DEVELON Adds New Forestry Equipment

- PACCAR Now Offers Allison Neutral At Stop Standard

- Wirtgen Presents Next Generation WR Series

- Euro Auctions Acquires Associated Auto Auction

- Kenworth To Address Diesel Technician Shortage

- FAE Introduces SAE Universal Attachment Plate For RCU75

- Komatsu Introduces 951XC-1 Harvester

- ProStack Launches TW 36-150 Telescopic Conveyor

- Ammann Unveils New Add-On Compactors

- New D-Series Mini Excavators From New Holland

- Trailer Manufacturer Showcases Products

- New Mack Anthem Now Available To Order

- Takeuchi Introduces New TL11R3 Compact Track Loader

- Doppbasket System Redefines Versatility For Doppstadt Inventhor

- Quadco Now Carries Bracke T26.b Disc Trencher

- DEVELON Introduces Powerful New Material Handler

- Eco Log Introduces New 688G Harvester

- Vermeer Unveils Electric Tree Care Equipment

- Keep Your Equipment Safe With Allu Tracker

- From Potatoes To Glass And Everything In Between

- Link-Belt Excavators Appoints JT Equipment As Authorized Dealer

- Supply Post October 2025 Issue – Read it now!

- Meet Hercules: The Heavy-Duty Telehandler

-

September

- VMAC to Showcase Multiple New Products at The Utility Expo 2025

- Mammoet Successfully Relocates Historic Church

- Bobcat Launches New Equipment At The Utility Expo 2025

- New Cat 980 GC Wheel Loader Delivers High Performance

- CASE To Showcase At The Utility Expo 2025

- OZ Lifting Showcases New Stainless Steel Davit Crane

- A Trucker's Tale – Hot Load!

- Komatsu Introduces New Excavators

- Turning Forestry Waste Into Industrial Fuel

- Seaspan Unveils New State-of-the-Art Operations Centre at Vancouver Drydock

- FAE Upgrades SSM Forestry Tiller

- John Deere Debuts Snow Removal Mapping

- JLG Expands ClearSky Smart Fleet IoT Platform

- NORCAT Selected To Advance Telecom Integration In Mining

- Dynaset Hydraulic & Electric Solutions For Farms

- Nova Scotia Updates Critical Minerals Strategy

- Feedback Wanted About Proposed Changes To PEI Off-Highway Vehicle Act

- Ontario Leads G7 With First Small Modular Reactor

- Euro Auctions Group Continues Expansion With New Acquisitions

- Vermeer Launches Tracked HG4000TX Horizontal Grinder

- Peterbilt Introduces New Front Frame Equipment Mounting Package

- ProStack Launches 150ft Conveyor

- Mack Trucks Delivers First Mack LR Electric Refuse Vehicle

- Elgin Sweeper Introduces Advanced Digital Control Panel For Pelican Sweepers

- CIB Announces $194 Million Partnership With JOLT

- FAE Updates Fixed-Tooth Mulcher For 5-Ton Excavators

- Lessons from Quebec: Flexibility Could Drive EV Progress

- Eaton And Chargepoint Establish Industry-First EV Charging Partnership

- Mack Introduces New MD Electric Bucket Truck

- ML-Truck Equipment Announces Opening Celebration

- National Heavy Equipment Show is Celebrating 30 Years Strong of Industry Power!

- Volvo Construction Wins Award For New Electric Design

- Hyster Expands Lineup Of Electric Forklifts

- FAE Enters Rotary Cutter Market With The New RCM/SSL

- Ammann Unveils Electric-Drive Reversible Plate Compactor

- Fed To Delay and Review EV Sales Mandate

- Allison Transmission 3000 Series Now Available with CNG-Powered Mack Granite

- Ballard Announces 1.5 MW Fuel Cell Engine Order For Sierra Northern Railway

- JLG Adds New Micro-Sized Scissor Lifts

- New All-Electric CBG 500 E Transshipment Cranes For Associated Terminals

- Meet The All-Electric 856HE MAX Wheel Loader From LiuGong

- Alberta Rejects Fed EV Mandate

- Peterbilt Launches Model 579EV And All-New Model 567EV

- International Introduces eRH Series Electric Trucks

- Supply Post September 2025 Issue – Read it now!

-

August

- Hamm Introduces HX 70e Battery-Powered Electric Tandem Roller

- Mean Green Introduces First Commercial-Electric Stand-On Autonomous Mower

- AUSA Unveils Electric Rough Terrain Forklift And Reversible Dumper

- First Diesel Trolley Power Agnostic Truck From Komatsu

- Ballard To Supply Fuel Cells To Samskip Vessels

- Gasoline Out Of Thin Air?

- The Rising Demand for Used Forestry Equipment in British Columbia

- Volvo CE Debuts Two Mid-Size Electric Machines

- Mecalac Launches es900tele Electric Telescopic Swing Loader

- Atlantic Heavy Equipment Show Celebrates 40 Years in Gear!

- FLO Components Ltd. Promotes Roger Freitas to Director of Operations

- Challenge Accepted: Fully Electric Telescopic Lifts From Faresin

- Island Yarder Gets Amped Up

- ESS Limited Expands Toronto Service Shop

- Building For the Future…Now!

- A Trucker's Tale – It’s Your Tie-Ya! (Tire)

- How to Sell Your Equipment on Supply Post

- History ReBoot 4.0: The Edison Motors Story

- Compact. Versatile. Quiet. Fully Electric!

- Heavyweight Matchup: The T-24D Trailer and Directional Drills

- Cat Introduces New Single Life Cutting Edges

- John Deere Launches New 510 P-Tier Excavator

- Merritt Acquires Magnum Trailer & Equipment

- MICHELIN Launches New X-CRANE 2 Tire

- Terex Ecotec Adds New Windrow Turner Range

- Top 10 Skid Steer Attachments For Maximum ROI

- July 2025 Canadian Equipment Market Report

- Keeping Streets Clean In The Summer

- Fassi Introduces New F705R.2-HXP-TECHNO Crane

- Hyster Adds Pedestrian Awareness Camera

- KIOTI Introduces Flow+ System For Compact Loaders

- Manitoba Invests In Three New Waterbombers

- Felling Trailers Awarded Cooperative Purchasing Contract With Canoe

- Kenworth Expands PACCAR TX-12 PRO Auto Transmission Availability

- New JLG Rapid Replaceable Platform Now Standard on Select Boom Lift Models

- New High Performance Circle For Cat Motor Graders

- Top 5 Challenges Facing Canadian Contractors in 2025 and How Equipment Choices Can Help

- Alberta Invests In Technology Transforming Tailings Ponds

- Choosing The Best Boom

- Komatsu Debuts New TimberPro Swing Machine

- Metso Introduces Enhanced Copper Electrorefining Technology

- John Deere Updates P-Tier Loaders

- FAE Upgrades PT300 Tracked Carrier With New Head

- Tips for Safely Transporting Heavy Equipment Across Provinces

- Daily Heavy Equipment Inspection Checklist

- Big Results: Microtrenching With Guzzler MT

- Supply Post August 2025 Issue – Read it now!

-

July

- New W100D Compact Wheel Loader From New Holland

- EDGE Innovate Launches New SCREENPRO S16

- Cat Upgrades Medium Wheel Loaders With Collision Warning System

- Alberta To Grow Manufacturing

- Revenue-Generating Summer Jobs For Land Contractors

- 5 Facts About Liebherr Wheeled Excavators

- Diesel vs. Electric Heavy Equipment in Canada

- Four New Mini Excavators From CASE

- VMAC Showcases Lean Expertise

- Brandt Opens New Winnipeg Facility

- 6 Unique ADT Uses Beyond Mining And Quarrying

- What Makes a Great Equipment Listing? Photo, Price & Copy Tips

- Finlay Unveils Transport-Friendly J-1280 Jaw Crusher

- Distinction Aluminum Hoppers Get Upgrade From Lode King

- Brokk Introduces New 130+ With Smart Power+

- John Deere Launches New H Series Forestry Machines

- Potain Tower Cranes Support $3B Skytrain Project in BC

- Waratah Launches New H427 Harvester Head

- Forestry Equipment Maintenance: Essential Tips for Maximizing Equipment Longevity and Performance

- MDS M515 Redefines Rip Rap Processing In North America

- Manitoulin Transport Delivers Life Saving Pet Food To Wildfire Affected Communities

- Mack Trucks Introduces All-New Mack Anthem

- HD Hyundai Announces Merger Of Construction Equipment Divisions

- Kenworth Chillicothe Plant Hosts Fourth Annual Kenworth Truck Parade

- Vermeer Launches New MTR516 Microtrencher Attachment

- Brandt Introduces New Heavy-Duty Material Handler

- A Trucker's Tale - A Tale of Good Cops

- How to Choose the Right Excavator Attachment for Your Job: A Complete Guide

- Stellar Debuts Heavy-Duty Tire Service Solutions

- Manitoba Invests $6.1 Million For Highway Reconstruction Project In Powerview

- GINCOR Werx Named One Of Canada’s Best Managed Companies For Third Consecutive Year

- Liebherr Tower Crane Lifts Steel Components For Giant Witches Broom

- Via Rail Launches Locomotive Engineer Apprenticeship Program In Northern Manitoba

- Peterbilt Adds TX-12 PRO Automated Transmission To MX-13 Engines

- Wirtgen Introduces SP 33 Slipform Paver

- First Two Replacement Cranes Arrive At GCT Deltaport

- CASE Beefs Up Large Excavator Lineup With New CX380E

- Vermeer Adds Triple Mowers

- June Market Insights: Canadian Equipment Market

- More Sand And Gravel, Less Red Tape For Alberta Aggregates

- Caterpillar Announces Excavator Upgrades

- Madill Returns to U.S. Market with First Sale of Upgraded 4000 Log Loader

- Wabash To Modernize Transportation Manufacturing With AI

- Kenworth Announces New T880S Performance Hood

- The Future of Heavy Equipment Rentals in Canada

- Firefighter Training Underway Ahead Of 2025 Wildfire Season

- Volvo CE Building Tracks At World RX

- Edge TRM831 Trommel Screen Boosts Productivity For Recycler

- DEVELON Introduces Its Next-Generation Log Loaders And Road Builders

-

June

- Manitou Launches New Scissor Lifts

- Supply Post July 2025 Issue – Read it now!

- New Actions To Power A Clean-Energy Future In BC

- DICA Introduces New EcoMax Crane Pads

- Alberta Heavy Equipment: Top Construction Industry Trends

- How Western Star is Making Trucking Cool Again to Attract New Drivers

- Bobcat Introduces New High-Capacity Diesel Pneumatic Tire Forklifts

- Holcim Acquires Langley Concrete Group Inc.

- Euro Auctions Group Acquires North Toronto Auction

- ProStack Adds New Range Of Tracked Conveyors

- FAE Launches New Mulcher For Excavators

- Heavy Equipment Auctions in Canada: A Complete Guide

- Metso Opens New Service Center In Western Canada

- CASE Adds Two New Midi Excavators

- Guide to Buying Used Dump Trucks in Canada: What to Look For

- Lode King Launches 2026 Renown Series Trailers

- Introducing The 7000XTDS Harvester Head From Quadco and Log Max

- Eighth-Generation Farmer Restores 1984 Mack R

- Cummins Introduces The X10 For 2027

- Selecting the Right Heavy Hauling Trailer in Canada

- A Trucker's Tale – Finished Lumber

- Equipment Sales & Service Limited named one of Canada’s Best Managed Companies

- Link-Belt Launches Payload Assist App

- Low-Carbon B.C. Nickel Will Bolster Canada's EV Battery Supply Chain

- Manitoba To Require NSC Numbers Starting July 1

- Road Safety Near Large Commercial Vehicles

- Electric-Drive Paver Grabs Attention At Bauma

- Pratt & Whitney Canada Selects Latecoere For Hybrid-Electric Demonstrator

- May Marketing Insights: The Latest Heavy Equipment Trends

- Vale Recognized For Safety Record

- Greater Sudbury Showcases Strong Indigenous Partnerships & Mining Excellence

- Peterbilt Showcased Advanced Technology Solutions

- Hyster Adds Hyster Tracker As Standard Feature On Broad Selection Of Lift Trucks

- More Lifting Power For Alberta

- Accelerating The Canadian Rare Earth Supply Chain

- Comparing Compact Track Loaders vs Skid Steers: Which is Best for Your Project?

- CASE Launches Five New Machines

- RCT Smart Technology Selected By Teck Resources

- Metso Launches Handling Systems For Stirred Mill Media

- Supply Post Attends Liebherr Demo Day 2025

- Terravest Acquires Tankcon

- Cat Introduces New MH3032 Material Handler

- Conveyor Design: The Backbone Of An Efficient Crushing System

- New Mine Will Create Hundreds Of Jobs In Northern Manitoba

- Meet The 2026 Distinction Super-B From Lode King

- Kenworth Announces Sunset of the Iconic W900, T800, and C500 Models

- Finlay Introduces New 883+ Electric Scalper

- Genesis Announces GXT EVO Mobile Shear

-

May

- How to Sell Heavy Equipment Fast in Canada: 5 Proven Strategies

- Supply Post June 2025 Issue – Read it now!

- Metso Launches New Nordberg HPe Series Cone Crushers

- Superior Patents Recirculating Conveyor On Sentry HSI Plant

- Sandvik To Supply Largest-Ever BEV Fleet

- Volumetric Concrete Manufacturer ProAll Launches Global Expansion

- Using Recycled Crushed Aggregates In Linear Infrastructure

- Kenworth Unveils W900 Legacy Edition

- Bobcat Adds Two New Tractor Models

- Volvo Launches New Generation Of Wheel Loaders

- VMAC Delivers Air Compressor Systems For Mining Applications

- New Report Reveals Contamination and Tailings Risks at Red Chris Mine

- Simex Introduces New Attachments At Bauma

- How to Inspect Used Excavators in Canada

- A Trucker's Tale - College Trucking

- EvoQuip Launches Its First Trommel

- Cargobull Upgrades TRUs

- Solving Farm Land Scarcity With Rooftop Greenhouses

- Vermeer Introduces Verifier G1 Utility Locator

- John Deere Introduces Two New Direct Hitch Scraper Models

- FAE Introduces Multipurpose Demining Arm

- 70+ Projects To Support Forestry In BC

- Next-Level Automation For Superior Cones

- Manitoba Government Partnering With Mining Association Of Manitoba Inc. To Grow Critical Mineral Market

- Canadian Sales Of Agricultural Tractors & Combines Grow

- BC Wildfire Service Has Record Application Numbers Ahead Of Wildfire Season

- Navigating Equipment Financing: How to Secure Loans for Heavy Machinery

- Krokodile Mobile Shredder: Revolutionizing Disaster Cleanup

- New Mini Brush Cutters From Diamond Mowers

- CBI Launches ChipMax 364T Whole Tree Chipper

- Bobcat Adds New Heavy Construction Equipment

- April 2025 Marketing Insights

- Big Rigs, Big Action: 2025 Atlantic Truck Show Hits Moncton Coliseum Today

- Cat Introduces New 775 Off-Highway Truck

- Newly Redesigned Flail Mower Attachment For Skid Steers

- Liebherr Announces Demo Days This June

- Terex Ecotec Promotes Cancer Awareness With Custom Blue TDS 815 Shredder

- John Deere Introduces Skidder Transmission Assurance Program

- Hydron Energy Announces Equity Investment from Modern Niagara Group

- PEI Receives Final Report From Forestry Commission

- Meet The New RQL/HY Forestry Mulcher From FAE

- Seaspan Begins Construction On Heavy Polar Icebreaker

- McCloskey International Celebrates 40 Years

- Doepker Acquires Peerless And Scona

- Jardine Auctioneers Becomes Part Of Euro Auctions Group, Joins Forces With Michener Allen Auctioneering

- Mammoet Breaks Record For Heaviest Transport In Alberta

- Supply Post May 2025 Issue – Read it now!

- BCCA Announces Launch of Construction Education Fund

- CBI Unveils New 5900T Horizontal Grinder

-

April

- Leading Resource Industry Expo Returns To Northern BC

- The Fecon Bull Hog: The Ultimate Mulching Machine For Land Clearing

- Caterpillar Introduces New FM528 GF/LL Forest Machine

- Thousands of Industry Professionals Gathered at Debut Alberta Equipment Expo

- Waratah Launches Forestry Grapple Line

- Automated Leader-Follower Platooning On Forest Roads Test A Success

- Tigercat Launches New Steep Slope Carriers

- Komatsu Announces New TimberPro TN230D Log Loader

- John Deere Updates Select Forestry Equipment

- Ponsse Introduces New Greasing System For Forestry Machines

- Hello, Hydrema!

- Bauma, Bauma, Bauma!

- A Trucker's Tale – Seabee Memories

- The Inaugural 2025 Alberta Equipment Expo Is Here!

- March 2025 Marketing Insights

- Peterbilt Introduces New LED Pod Headlights For Model 589

- Tommy Gate Now Offers Lifting Solution For EVs

- Terex Recycling Systems Launches TDS-820SE Low Speed Shredder

- Volvo Introduces Straight Boom For Electric Mini Excavator

- MAGNA Expands Offering with Swiss-Engineered GIPO Products

- Updates To Eagle Iron Works Classifying Tanks

- New Vermeer Bit Boss System Advances Bit Retention For HDD

- Bobcat Debuts B760 Backhoe Loader

- Cooper Equipment Expands With New Acquisitions

- Purchasers And Lessees Of Certain Hino Trucks Sold In Canada May Qualify For $55M Class Action Settlement

- Seaspan Invests $2.5 Million In Indigenous Shipbuilding Training

- Hangcha Forklift Canada Secures Major Contracts

- NASCAR Depends On Elgin Sweeper

- Caterpillar Releases Limited Edition Machines To Honour Centennial

- BOMAG Introduces New Paving App

- Mack Trucks Celebrates 125 Years

- CASE 580EV Electric Backhoe Loader Earns Award

- John Deere Adds All-New Dozers

- Volvo Launches Five New Hybrid Excavators

- Caterpillar Introduces New 789D Autonomous Water Truck

- HX90A Tops Hyundai’s Compact Excavator Line

- Mecalac Unveils The Revo990 Backhoe Loader

- Forests Canada Announces Award Winners

- Seaspan’s Welding Centre of Excellence Lab Obtains ISO Accreditation

- Alberta Tax Credit Fuels Bioprocessing Industry

- Sandvik Introduces New D50KX Drill Rig

- Screed Configurator For Pavers Now Available From Dynapac

- New Tadano AC 5.250L-2 All Terrain Crane

- Supply Post April 2025 Issue – Read it now!

- VMAC Unveils e30 Battery Electric Powered Rotary Screw Air Compressor

-

March

- Revolutionize Waste Management With LiuGong

- Cat Releases New 395 Long Reach Excavator

- LNG-Powered Ships Can Now Fuel Up At The Port Of Vancouver

- JCB Celebrates One Million Backhoes

- Liebherr Launches New PR 776 Generation 8 Crawler Dozer

- Brokk Now Dealer For SHERPA Mini Loaders

- The Unique Industrial Value Of The Articulated Hauler

- Sany Rough-Terrain Crane Featured In New Operator Program

- Hitachi Is Back With New Compact Line-Up

- Immigration Plays Critical Role In Construction Sector

- Horizon Aircraft Sees Growing eVTOL Interest From Military

- Haver & Boecker Niagara Showcase Full-Size Portable Plant

- CM Labs Expands Walkaround Inspection Packs

- MAJOR Introduces Advanced Screen Media Technology

- Foreman Equipment Welcomes Wash Recycling Expert Tim Best

- Velocity Truck Centres Expands Footprint With New Branch Opening In Kelowna, BC

- A Trucker's Tale – Military Projects, A Gallery

- Watch for our April Issue!

- Palfinger Launches New P6 Radio Remote Control

- Alberta Levies New Electric Vehicle Tax

- Epiroc Launches New DTH 5 Hammers

- Engcon Launches New Tiltrotator

- The Power Behind Geothermal Drilling

- Genie Debuts New Boom Lifts

- Canadian Crane Service Adds New LTM 1160-5.2 To Fleet

- Six Ways Rokbak Trucks Make Operating Straightforward

- Cedarapids TI4250 Horizontal Shaft Impactor Now Available

- New Range Of Overhaul Kits For Perkins 2000 Series Engines

- Metso Releases New Power Unit For Nordberg MP Cone Crushers

- New 250E Loader From Tigercat

- Process Challenging Waste With The VS420 Shredder From Edge Innovate

- Genie Launches New Telehandlers

- New B.C. Council Will Advocate For Forestry Workers

- Bobcat Of Vancouver Joins Bobcat Company Dealer Network

- Now Is The Time To Shop Canadian!

- Resilient Supply Chains: Meeting The Challenges Of A Changing North America

- Purolator Acquires Livingston International

- Keestrack Showcases New Machines At Bauma

- Verne Achieves Hydrogen Storage Milestone

- Volvo Unveils Brand New Lineup Of Articulated Haulers

- New Holland Introduces New TH6.26 Compact Telehandler

-

February

- Supply Post March 2025 Issue – Read it now!

- Canada Cartage To Acquire Walmart Fleet

- Kubota Celebrates 50 Years In Canada

- Rare Vintage Wheels Roll Into Alberta Museums

- Tigercat Launches 120 Winch Assist

- Expo Grands Travaux Returns To Saint Hyacinthe This Spring

- CPKC Orders Ballard Fuel Cell Engines For North American Locomotives

- Nors Promotes Roadshow In Canada To Reinforce The Launch Of The Global Brand

- DC Equipment Showcases Iconic Brand Madill

- Lode King Updates Prestige Super-B Trailer

- Preparing Your Business For Potential Tariffs: What You Need To Know

- Finlay Introduces C-1550+ Tracked Cone Crusher

- A Trucker's Tale – The Last Hoorah

- Low-Value Wood Waste Generates Benefits For Fort St. James

- JLG Announces New JLG 519 Telehandler

- Liebherr Delivers 1,000th Airbus A220 Landing Gear Brace

- Tigercat Releases LX877 Feller Buncher

- Volvo CE Adds Two Mid-Size Excavators

- Mullen Ramping Up US Battery Production

- Metso Introduces Integrated Copper Electrowinning Plant

- Bobcat Machine IQ Remote Engine Security Feature Available Across Additional Equipment

- Mecbo America Launches Beton Cap Concrete Mixer-Pump

- Manitoba Plans Multi-Year Infrastructure Investment Strategy

- Clean Carrier Program Achieves Significant Reductions

- CN Launches New Medium Horsepower Hybrid Locomotive

- Cummins Launches New 6.7L Turbo Diesels

- New Scavenger Wash Circuit From Superior

- Great Dane Commemorates 125 Years In Transportation

- BC Supports Forest-Sector Manufacturing

- OZ Lifting Relaunches Tele-Pro Davit Crane

- Essential Tips For Preparing Your Street Sweepers

- New Cat D8 Dozer Provides Next-Level Technology

- Mecalac Launches 3 New Compact Excavator Models

- Pettibone Introduces Extendo 1536X Telehandler

- New Powerful Cedarapids Static Cone Crusher

- Supply Post February 2025 Issue – Read it now!

-

January

- Caterpillar Adds 20 kVA Mobile Genset

- Manitoulin Transport Opens New Terminal In Alberta

- LBX Company Announces 370 X4S Excavator

- Fassi Releases New F2350RL-XHP Techno

- John Deere Showcases New Autonomous Tech

- Maximize Winter Work For Land Management Pros

- Caterpillar Launches New Telehandlers

- Nors Appointed Exclusive Volvo CE Dealer For Manitoba

- Metallica Inspires New CASE Compact Track Loader

- Mecalac Brings Revotruck To North America

- Kubota Adds Three New Compact Models

- Brandt Gives $550,000 In Donations

- Western Star Transports Martin Mars Bomber

- Edmonton Set To Welcome Inaugural Alberta Equipment Expo

- The Ultimate 2025 Trade Show List!

- A Trucker's Tale – Autocars and The Missing M16

- Yanmar Launches New Line of Branded Attachments For Compact Track Loaders

- Terex Recycling Systems Launches TSD-280 Drum Screen

- Mecalac Launches New Range Of Hammers

- MDS Launches SCRAPMASTER 400

- Plug And Play Joins Forces With Daimler Truck North America

- Utility Now Offers Lightweight Brake Drum Standard On All Models

- Vermeer Introduces Compact, Efficient MX150 Mixing System

- John Deere Rolls Out SmartDetect For Loaders

- Wheaton Precious Metals Launches $1 Million Future of Mining Challenge

- Hardox HiAce Doubles Service Life Of Reclaimer Buckets

- TJ Hunt Trucking Improves Efficiency With Kenworth T880s

- Mullen Announces Refrigerated Solution For Class 3 EV Truck

- Lippmann Welcomes Tyalta As Newest Dealer

- Yanmar CE Launches New Zero Tail Excavators

- How To Choose The Right Forestry Mulcher

- The Tech Dilemma Facing Dealers

- Latest New Holland CR11 Combine Harvester To Be Fitted With Two Extraordinary New Tires

- Takeuchi Manufactures 10,000th CTL

- Fastfrate Group Opens New Facility At Centreport Canada Rail Park

- AME Announces 2024 Award Recipients

- Erkat Celebrates 25 Years Of Innovation

- New, Lighter 544 Harvesting Head From Tigercat

- John Deere To Integrate Trimble SmartGrade Tech

- Volvo CE Upgrades Straight Boom Demolition Excavators

- JLG Introduces New E313 Electric Telehandler

- Yanmar Launches New TL65RS Compact Track Loader

- FAE Releases New SFL Multitask Head For Tractors

- Canada Cartage Acquires Coastal Pacific Xpress

- Perkins Launches New 2600 Series 13-Litre Engine

- Supply Post January 2025 Issue – Read it now!

-

December

-

2024

-

December

- Superior Updates Telestacker Conveyor Automation

- Meet The New E90D Midi Excavator From New Holland

- Labatt Invests $5.47 Million To Expand Fleet In Quebec

- MDS Launches New M300 Scalping Screen

- Upcoming Supply Post Office Closures

- Genie Launches Six New Scissor Lifts

- Komatsu Introduces New WA700-8 Wheel Loader

- Quadco Launches The M52 Drum Mulcher

- CASE Introduces Limited Signature Edition Backhoe Loader

- Kenny's Loggin' – A Hip Replacement

- Tigercat Officially Launches 6500 Chipper

- Volvo CE Launches New High Reach Excavators

- A Trucker's Tale – Good Food

- New Holland Launches New E70D Midi Excavator

- Eaton Expands Montreal Innovation Center

- VMAC Launches High-Voltage Electric Vehicle Business

- Meet The New RT-65 Compact Track Loader From ASV

- City of Houston Purchases 15 Gradall Excavators

- Hyster Announces Latest Electric Forklift

- New Extended-Reach 326 P-Tier Telescopic Wheel Loader From John Deere

- Forests Ontario Planted 2.7M Trees Across Canada This Year

- AMTA Collaborates On Zero Emission Truck Testbed

- New Swinging Hammer Mulcher From FAE

- How Safety Training Improves Operational Efficiency in the Canadian Trucking Sector

- New BC Ferries Will Not Be Built in BC

- Sustainable Forest-Sector Manufacturing Jobs Coming To BC

- Manitoba To Invest In Wind Generation

- New Mid-Size Articulated Loaders From New Holland

- EvoQuip Celebrates 1500th Machine

- Air Burners: A Game-Changer In Wood Waste Management

- MAJOR Introduces New Advanced Polyurethane Strip Variant

- SCREENPRO S18 Touches Down In North America

- Vermeer Launches PD25R Pile Driver For Solar Field Construction

- Waratah Launches New HX Harvester Heads

- Innovative Uses For MB Crusher Attachments

- Hyundai Introduces HD130 Dozer

- Liebherr Wheel Loaders Are Versatile In Snow And Ice

- Supply Post December 2024 Issue – Read it now!

-

November

- International HV Raises the Bar For Vocational Work Truck

- Loftness Introduces Lightweight Battle Ax Mulching Head For Compact Excavators

- Vermeer Unveils The D24 Horizontal Directional Drill

- Yanmar Introduces New ViO35-7 Mini Excavator

- New Long Front Excavators From LBX

- Bobcat Introduces TL623 Telehandler

- Peterbilt Supports United Way With Annual Parade

- Freightliner Unveils Fifth Generation Cascadia

- Strongco And Great West Equipment Unite Under The Nors Brand

- Cat Introduces 903 Compact Wheel Loader

- Brandt To Liquidate Truck Leasing Firm Fleet Assets

- John Deere Commemorates 75 Years Of Dozer Innovation

- 2024 Supply Post Christmas Shopping Guide

- Festive Lights Return To Vancouver Island Streets

- A Trucker's Tale – Concrete, Jackhammers, And Absurdities

- Kenny's Loggin' – Breaking and Sorting Bundles

- Volvo CE Adds New Electrified Models

- Yanmar Introduces TL75VS Midsize Compact Track Loader

- PEI Introduces Mandatory Class 1 Commercial Truck Driver Training

- Yuck! What Are Fatbergs In Sewer Systems?

- New BL1/EX-75 Forestry Mulcher From FAE

- Accelera By Cummins Awarded $75M For Zero-Emissions Manufacturing

- Utility Trailer, Cargobull North America Unveil New Liftgate Battery Charger

- Ballard Launches Latest Fuel Cell Engine For Heavy-Duty Vehicles

- Hendrickson Acquires Reyco Granning

- Eaton Introduces 48-Volt DC/DC Converter Designed For Harsh Environments

- Stellar Debuts New Aluminum Option for TMAX 3T Mechanic Truck

- Hyundai Adds New Excavators

- Caterpillar Launches New Compact Loaders

- Gearmatic Introduces GM12A Planetary Hoist

- Volvo CE Adds New 12-Ton Soil Compactor

- Haul Track Helps Customers Get More From Their Rokbak Truck

- Metso Launches MX For Cones

- BOMAG Introduces Emergency Brake Assist

- DEVELON Opens New Customization Plant

- OTR Introduces Three-Piece Forestry Wheel

- Cat Brings Mine-To-Mill Vision To Life With New Tools

- Tigercat Launches New 234C Knuckleboom Loader

- New FAE App Offers Real-Time Machine Data

- Elgin Sweeper Releases DualEyes On RegenX

- Supply Post November 2024 Issue – Read it now!

-

October

- CASE Introduces Custom Compact Track Loader Wraps

- Liebherr Premieres PR 776 Generation 8 Crawler Dozer

- Velocity Acquires Autow Nationalease Truck Rental

- Metso Acquires Diamond Z And Screen Machine

- MDOT Lifting Restrictions For Ambassador Bridge

- Brandt Named Exclusive Canadian Dealer For ClearEdge3D Products

- CPKC Unveils 2024 Holiday Train Schedule And Artist Lineup

- Firestone Ag Introduces Premium Bridgestone Tractor Tires

- The Groundworx Co Honoured With Award

- FLO Components Ltd Earns 2023 Lincoln Distinguished Distributor Award

- Celebrating 75 Years of Inland Truck & Equipment: A Legacy of Innovation and Service

- Frontline Machinery Brings CBI To Eastern Canada Network

- Kennys Loggin – On Strike!

- A Trucker's Tale – It Was What It Was

- Takeuchi Brings TCR50-2 Crawler Dumper To North America

- Peterbilt Announces Largest Electric Vehicle Order To Date

- DEVELON Introduces Its Smallest Mini Excavator Yet

- Mecalac Launches New 12MTX Wheeled Excavator Loader

- Meet The Electric Vehicle Line-Up From Navistar

- Vermeer Introduces Enhanced RTX1250 Ride-On Tractor

- Accelera Launches Next-Gen Hydrogen And Electric Solutions For Commercial Vehicles

- Hiab Expands Spare Parts Portfolio

- Stellar Showcases Next-Generation Hooklift Innovations

- Bendix Tech Tips: Air Dryer System Inspection

- Mastering The 856H LiuGong Wheel Loader

- Klein Unveils New Model K400SS-TD Water Truck

- New FCmove-XD Fuel Cell Engine From Ballard

- Alberta Turns Waste Into Electricity

- How Is Reduced-Temperature Asphalt Produced?

- CLARK Returns To USA

- DEVELON Rolls Out DX100W-7 Mini Wheel Excavator

- Komatsu Brings Demolition Excavators To North America

- Seaspan Launches New Science Vessel

- Takeuchi Brings TB395W Wheeled Excavator to North America

- New Telescopic Reach Small Articulated Loaders From New Holland

- Highway Motor Freight Expands Operations At Centreport Canada Rail

- Mack Refreshes Mack MD Series

- Mecalac Launches The Revotruck: The Safest And Most Ergonomic Dumper On The Market

- Isuzu Starts Production For All-New NRR-EV

- KOBELCO Unveils the New SK520LC-11 Excavator

- Volvo Upgrades Two Popular Mid-Size Wheel Loaders

- Hyundai Adds New HX-A Compact Excavators

- Supply Post October 2024 Issue – Read it now!

-

September

- Hitachi Introduces ZAXIS-7 Super Long Front Excavator

- Bobcat Introduces New Utility Tractors

- Astec Upgrades Fiberbed Mist Collector With Charcoal Filters

- Go Green With An Electric Waste Shredder

- Metso Expands To Prince George

- Superior Adds New Conveyor Impact Cradles

- Dana Spotlights Next-Generation Drive and Motion Mining Technologies and New Certified Reman Program at MINExpo

- Greater Sudbury Showcases Mining Excellence at MINExpo 2024

- SRC Rare Earth Processing Facility First to Produce Rare Earth Metals in North America

- Meet The New Cat 6020 Hydraulic Mining Shovel

- All-Electric Operation Of Mobile Crushing And Screening Plants With Kleemann

- JRayl Transport Moves To Kenworth T680

- TRANSTEX Acquires APU Manufacturer DClimate

- New John Deere Loaders Bring The X-Factor

- Terramac Launches Wheeled Dumpers

- Kennys Loggin – A Job Upgrade

- The Amazingly Versatile, Multi-Purpose Dump Truck

- New Cant Saw Technology From HewSaw

- How To Choose The Right Drum Mulcher

- FAE Updates Its Top-Of-The-Line Tracked Carrier: The PT550

- Heavy-Duty Brushcutter Conquers Tough Jobs With Ease

- New Cat Grading Beams Deliver High Productivity Material Grading

- Lafarge Canada and Hyperion Launch Tandem Carbon Recycling System

- Komatsu Launches Battery-Electric Drilling & Bolting Rigs

- Edmonton Agg Supplier Chooses Rokbak

- Epiroc Updates SmartROC Tophammer Cabin Rigs

- Sandvik Electrifies Its Largest Intelligent Rotary Blasthole Drill

- Astec Introduces Revolutionary Screening Technology

- CASE Launches Industry-First Electric Backhoe Loader

- Metso Crushes It With New XM Series

- Kenworth Chillicothe Plant Hosts Third Annual Kenworth Truck Parade

- The City of Kingston, Ontario, Orders Two Mack LR Electric Refuse Vehicles

- Carbotech Group Acquires Sawquip

- Manitou Adds Tree Saw Option For Telehandlers

- The Top Benefits Of Forestry Mulching

- BC Forestry Employers Need To Get Ready For New First Aid Requirements

- Tigercat Releases 6040 Carbonizer

- The Power Of Biomass Chippers And Grinders

- Supply Post September 2024 Issue – Read it now!

-

August

- OFIA Sees Growth In Clean Energy And Bioeconomy

- Efficient Vegetation Management For Effective Storm Cleanup

- Loftness Introduces New Stump Grinder Attachment

- New FAE BL2/S/EX Forestry Mulcher

- Alberta Supports Wildland Firefighting Heroes

- DC Equipment Canada Brings Madill Back To BC

- Mack Trucks Historical Museum Celebrates 40 Years

- New Commercial Vehicle Inspection Station Near Terrace

- Land-Clearing Business Finds New Revenue With Tigercat 6900 Grinders

- From The Archives:100 Mile House Mill Off To A Smooth Start

- New Manufacturing Jobs Coming To Castlegar

- Waratah Introduces New H216 Hardwood Head

- Logging Giants Get New Life

- WoodWorks BC Releases Alternative Solutions Guide

- A Trucker's Tale – Hauling Freight In Vietnam

- Alberta Equipment Expo Announces Official Show Guide Provider

- Kennys Loggin – The MacMillan Bloedel Family

- AED and CEDA Announce Upcoming Merger

- New Fuel Tank Isolation Valve For Hybrid EVs From Eaton

- AI To Spark 10-Year Critical Minerals Supercycle

- New Refuse Vehicles From Mack

- WattEV Opens Largest Solar-Powered Truck Charging Depot In World

- Alberta Is Calling Skilled Trades

- Cargobull Hybrid TRUs On Utility 3000R Are A Game-Changer

- Peterbilt Enhances Red Oval Certified Program

- Brokk Opens New Canadian Distribution Centre

- What Are Strategies for Mitigating Women Truck Driver Challenges?

- Terex Washing Systems Marks Five Years Of Manufacturing Filterpresses

- CDE Unveils New ProPress Filter Press

- Canada Updates Critical Minerals List

- Understanding Weigh Scaling Technology For Wheel Loaders

- JLG Updates SkyTrak 8042 Telehandler

- Cummins And Isuzu Launch Battery-Electric F-Series

- Hangcha Now Offers Lithium-Ion Powered Forklifts

- GTR Tiltrotators From GRYB Transform The Way You Work

- EvoQuip Introduces Bison 170 Jaw Crusher

- Epiroc Completes Acquisition Of Yieldpoint

- Supply Post August 2024 Issue – Read it now!

-

July

- OZ Lifting Launches Wireless Hoist Options

- MB Crusher: Crushing It In The World Of Infrastructure

- Kenworth Unveils SuperTruck 2

- Sustainable Cold Chain Solutions Are Possible

- EDGE Innovate Launches New VS750i Primary Waste Shredder

- Yanmar CE Introduces All-New Electric Trio

- New Holland + Bluewhite To Develop Autonomous Solutions

- International S13 Integrated Powertrain Already Hard At Work

- Mammoet Begins Assembly Of World’s Biggest Land-Based Crane

- Why Are Old Milling Machines Green?

- Hydrogen Refuelling Stations Coming To BC

- No Truck Parking: A National Safety Concern

- Hyundai Introduces HD100 Tracked Dozer

- Tips For Sewer Maintenance

- CASE Launches New Machines

- News from Supply Post!

- AMTA Celebrates 74th Professional Truck Driving Championship

- Terex Launches MAGNA For Large-Scale Operations

- DEVELON Introduces New DTL35 Compact Track Loader

- Lean And Green: The New EvoQuip Caiman 150 Compact Shredder

- Kennys Loggin – Tree Pullers, Sawlogs, and Conk Knots

- A Trucker's Tale – The Compactor Caper

- New Portable Nitrogen Membrane Generators From Atlas Copco

- Red Signals Confidence At Yanmar CE

- Cummins Launches X15 HELM Diesel Engine

- Cat Updates PM300 Cold Planer Series

- New RL-5K Off-The-Road Tire For Heavy Duty Loaders From Goodyear

- Bendix To Double Air Disc Brake Production Capacity

- Consultant Chosen For Eyremore Dam Study In Alberta

- Fort McKay First Nation And Suncor Energy Partner On Oil Sands Development

- Manitex Delivers New Articulated Truck Mounted Cranes

- Peterbilt Now Offers New Cummins X15N Natural Gas Engine

- TerraVest Industries Acquires Advance Engineered Products

- Port Of Vancouver Reports Record 2023 Trade Volume

- Recycling Construction And Demolition Waste Saves Money

- Caterpillar Updates Mid-Sized Asphalt Compactors For 2024

- What Is The Tiltrotator Effect?

- Terex Washing Systems Launching New Software System

- Astec Announces New Remix Cold Central Plant Recycling System

- How To Recover And Reuse Soil From Construction Sites

- Mack Begins Production Of Mack MD Electric

- Dynapac Launches New Multi-Function SD2500CS Protac Spray Paver

- Volvo Unveils New Excavators

- Finlay Launches Two New Models

- Supply Post July 2024 Issue – Read it now!

-

June

- BCCA Delivers Federal Funding For BC Construction Apprentices

- Metso Launches New Crusher Wear Products

- New 27-Inch Vacuum For Vactor 2100i Combination Sewer Cleaner

- The Quietest Vessel On BC Coast Is An Electric Tugboat

- Crushing Old Habits

- Oshkosh Corporation Acquires AUSA

- Furniture Delivery Electrifies With Kenworth K270E

- Manac Now Offers Smart Trailer Solution

- Case Upsizes Equipment For Landscaping

- Nine Essential Tips For A Great ADT Operator

- New 330 Straight Boom Excavator From Cat

- Brandt to Expand Material Handling Division Across Canada

- Engcon Launches A New Size Of Ground Compactor

- Navistar Delivers First International S13-Equipped LT Series To Fleets

- Kenny's Loggin – Supervising the Supervisors

- A Trucker's Tale – Trucks of the Past

- MDS Introduces T-Link Telematics System

- Sandvik Introduces New Push Bore Reamer System

- Canada Announces Over $15 million For Canadian Mining Sector

- Stellar Unveils Latest TMAX Mechanic Trucks & Accessories

- FAE Updates STCM Stone Crusher For Tractors Up To 280 Hp

- Genie Adds Access Deck To Popular Micro Scissor Product Line

- Dana Earns Top Employer 2024 Awards

- Genesis Introduces M7 Concrete Cracker

- Peterbilt Introduces New 72-Inch Sleeper For Model 589

- Superior Telestacker Conveyor Automation Now Easier To Use

- Eaton Adds Remanufactured Advantage Line Of Clutches To Its Portfolio

- Groupe Touchette Building New Distribution Centre At Centreport

- Terramac Crawler Carriers Go Global

- New Triangulated Harvesting Head From Tigercat

- Altor Locks Now Offers ICON Trailer Lock

- In-Cab Warning Devices Now Required In Dump Trucks: BC

- Thermo King Adds BlueSeal Air Curtains

- Women In Trucking Association Announces 2024 Drivers of the Year

- 4 Gen Logistics Adds Volvo VNR Electric Trucks To Fleet

- Trucking Job Vacancies Could Surge By 2030

- Peterbilt Delivers 520EVs To Anchorage Municipality

- Manitoba To Upgrade Roads In Norway House

- Hennessey VelociRaptoR 1000 Super Truck Now in Production

- New Learning Pathway For Alberta Class 1 Drivers

- Supply Post June 2024 Issue – Read it now!

-

May

- GreenPower Unveils New EV Star Utility Truck

- Stellar Opens Iowa Warehouse Facility

- DEMO International Heads To Ottawa This September

- FuelCell and Toyota Launch Tri-Gen System

- Urgent Need For Commercial Truck Driver Training

- Entrans And Drōv Technologies Extend Exclusive Partnership

- Navistar Drives Toward Autonomous Technology

- Velocity Truck Centres Breaks Ground On Kelowna Facility

- Peterbilt Introduces Innovative Digital Vision System-Mirrors

- Freightliner Produces Milestone One Millionth Cascadia

- Evergreen Waste Chooses Mack LR Electric Refuse Trucks

- Equipment Sales & Service Limited named one of Canada’s Best Managed Companies

- Peterbilt Introduces New PACCAR TX-8 Auto Transmission

- RCC To Address Empty Trailer And In-Transit Moves

- Kenny's Loggin' – Engineering at Menzies Bay

- A Trucker's Tale – Junnie Jones

- Superior Introduces New Heavy-Duty Scalping Screen For Large Feed Size

- New Holland Enhances GENESIS T8 Series Tractors For 2025

- Manitou Launches New MTA 519 Compact Telehandler

- New SCL/RCU Stump Cutters From FAE

- Manitoba Seeks Feedback On New Critical Minerals Strategy

- First Nations and Ontario Nearing All-Season Roads In The Ring Of Fire

- New Holland Marks 50th Anniversary Of Round Baler

- New Technology Reduces Environmental Impact From Mining

- MAC And The Copper Mark Collaborate

- Goodyear Introduces GP-3E Off-The-Road Tire

- WorkSafeBC Advances Crane Safety In B.C.

- Volvo CE Expands Range Of Straight Boom Demolition Excavators

- EDGE Innovate Reveals New SCREENPRO S18 Scalper Screen

- New Counterflow Drummix Plant From Ammann

- Tough Wildfire Clean-Up Made Easy With Sennebogen

- BC Continues Investments To Support Forest Sector

- New Hammermill Horizontal Grinder From Bandit

- Alberta Wildlife Is Ready For Its Close-Up

- FAE Introduces New C/3/MAX Tooth For Select Forestry Mulchers

- Wildfire-Damaged Wood Recovery Underway In B.C.

- New Mulching Head For Fire Mitigation From Tigercat

- Forestry Takes Action On Safety

- Vermeer Launches LS3600TX Low Speed Shredder

- B.C. Plants Its 10-Billionth Tree

- FLO Components Ltd. Announces Winner in NHES Lincoln 1888 PowerLuber Grease Gun Contest!

- Metso Launches Nordberg HP350e Cone Crusher

- JLG Introduces New ES4046 Electric Scissor Lift

- RIZON Trucks Arrive In Canada

- Menzi Muck Spotlighted At Canada's Largest Interior Logging Show

- Rubble Master: A Year of Remarkable Growth

- Supply Post May 2024 Issue – Read it now!

-

April

- Success Story: Edge Innovate FTS75 Mulch Master

- 6 Tips For Selecting The Right Traveling Axle Trailer

- Taking Wildfire Operations To New Heights In Alberta

- New 973 Rounds Out Updated Cat Track Loader Lineup

- Day of Mourning Honours Workers Lost On The Job

- New Holland Launches 3 New Compact Wheel Loaders

- Peterbilt Introduces New Car Carrier Models

- A Trucker's Tale – Flatbeds and Lowboys

- Kenny's Loggin' – Safety at Menzies Bay

- Epiroc To Acquire STANLEY Infrastructure

- Tigercat Opens New Parts Warehouse

- Yanmar Introduces New Compact Equipment Lineup

- Ballard Supplies 100 Fuel Cell Engines To NFI

- Frontline Machinery Acquires Lonetrack Equipment

- New Rugged Excavating Tool From Werk-Brau

- New Precision Laser From DEWALT

- New Safety Features For Western Star Vocational Trucks

- Brigade Launches New Collision Prediction System

- CPKC Announces 2024 Steam Tour Schedule Dates

- Beyond Borders: The Crucial Role of 24/7 Customs Brokers

- Fassi Adds F1250R-HXP To TECHNO Series

- Timmies Goes Electric

- Trucks For Change Network Showcased At Truck World

- Northern Touch Truck Wash Opens New Location in Fort Erie

- Canada Cartage Opens State-Of-The-Art Terminal In Alberta

- The Ultimate Trade Show, Forum & Conference List for 2024!

- Lost & Found: Trailer Technology Triumphs

- Peterbilt Cements Rugged Models 567 & 589 For Concrete Industry

- XL Specialized Trailers Launches New Knight Mfg Trailer

- Looking for older issues of Supply Post?

- CIB Commits $138.2M To NS Energy Storage Project

- First Crewtek Graduates Are Ready To Work

- CC Steel Relies On Vactor

- Cat Medium Dozers Receive Technology Upgrades

- How To Choose An Articulated Hauler

- CM Labs Launches Intellia Instructor

- Elvaan Redefines Standards At NHES 2024

- Bobcat Announces Lineup Of New Products

- John Deere Launches 950 P-Tier And 1050 P-Tier Dozers

- Yanmar CE Rolls First Compact Track Loaders Off the Line

- On-Site Refueling Gets Efficient

- Mats Unlimited And Williams Lake First Nation Join Forces In Access Matting Collaboration

- Bomag Introduces Remote-Control BMP 8500 Compactor

- Volvo CE and Mack Trucks Partner for Electrification Project

- Precision Utilities Utilizes Hydro-Excavation For Emergency Utility Work

- Caterpillar Launches New Safety Programs

- Powerscreen Unveils New Global Headquarters

- World’s First Cabinless Remotely Operated Electric Skid Steer

- Finlay Supports Cancer Fight With Custom Machine

- Metso Introduces Nordwheeler Portable Crusher

- Supply Post April 2024 Issue – Read it now!

-

March

- 5 Tips for Spring Street Sweeping

- Terex Unveils Ecotec TDS 815 Shredder

- Opportunities And Challenges Facing Women In Construction

- Komatsu Introduces GD955-7 Motor Grader To North American Market

- Construction Industry's Stance On Canada's Road Infrastructure

- Ontario-Made Hydrogen Power Generator Put To The Test

- FLO Components Holds Grease Gun Giveaway AT NHES

- Safety Tips For Operating Industrial Vacuum Trucks

- Grinding Adversity Into Opportunity: Tyalta Industries

- Kenny's Loggin' – You Can't Yard Like That!

- A Trucker's Tale – The Convoy Point